On Monday, August 9, 2021, the ‘Cloud 100’ list was announced. ‘Cloud 100’ is a list published by Forbes, together with Salesforce Ventures and Bessemer Venture Partners, covering the world’s top 100 cloud-based, private B2B companies by enterprise valuation.

The ‘Cloud 100’ of 2021 has a simple yet powerful message: ‘Cloud-based startups are stronger and faster.’

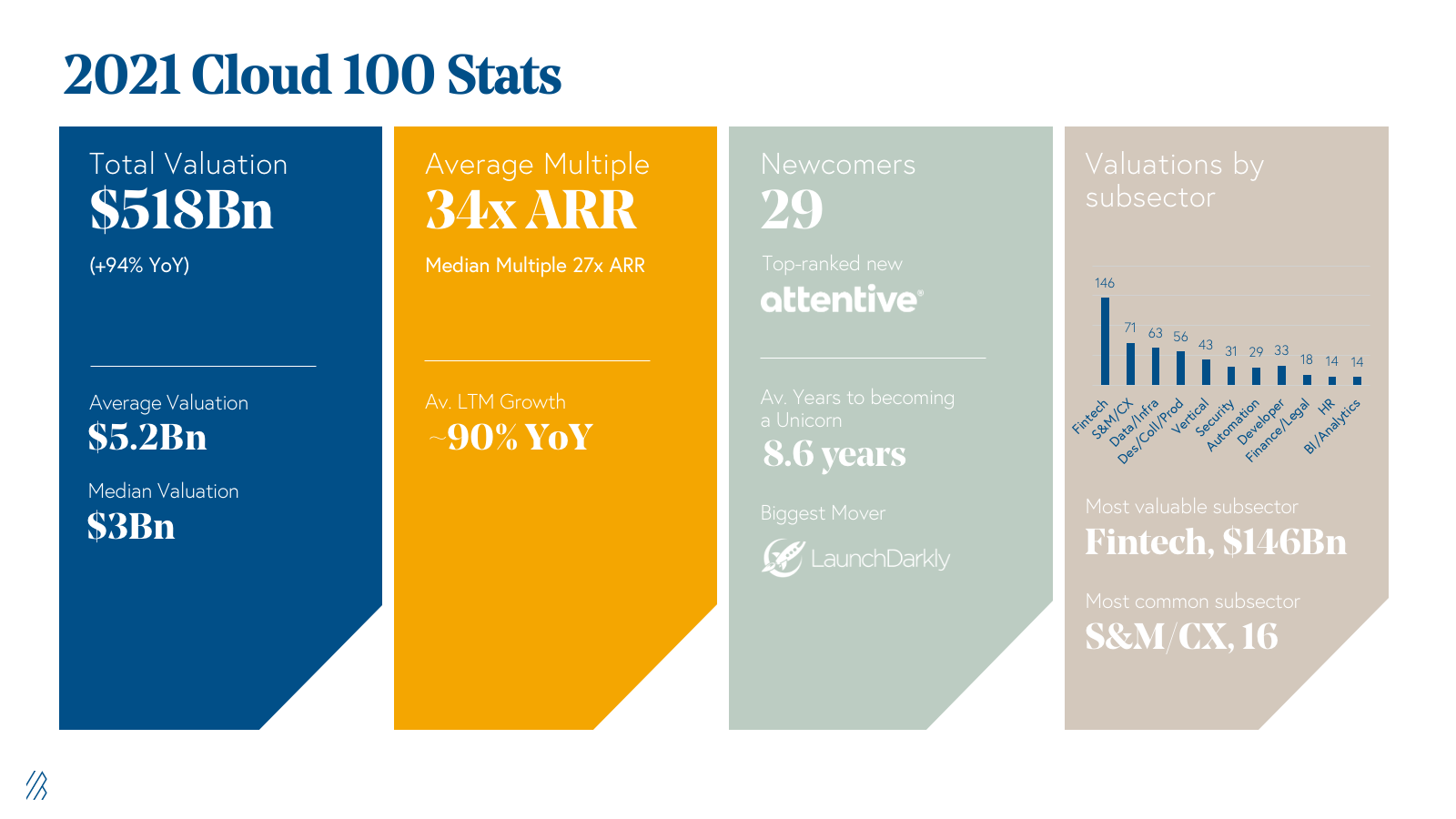

In other words, the valuations of the top 100 startups have nearly doubled compared to the previous year (the combined valuations of the top 100 companies in 2021 is $518 Bn, up about 94% from [JG1] 2020). In addition, cloud companies are being given a higher multiple on the same ARR (ARR multiple of x23), and the time to become a unicorn is decreasing. In 2016, when the ‘Cloud 100’ was first published, it took nearly 12 years to become a unicorn startup (about $1 bn), but in 2021—with the exponential growth of the cloud economy— it takes only 8.6 years to reach the same valuations

However, after reading the ‘Cloud 100’ list and related analyses, I thought it would be nice to have more in-depth insight for reference from the perspective of founders who currently run B2B or SaaS startups.

I’m an early member of a Silicon Valley-based startup called Sendbird, and since 2018, I’ve had the opportunity to look at business and go-to-market (GTM) trends for cloud and B2B/SaaS companies, along with various industry leaders. I would like to summarize the trends in the global cloud business over the past two years, starting in 2020—after the onset of COVID-19—which can be particularly interesting for our businesses.

The background of the unicorn surge in the cloud sector—valuations multiple per ARR increased by 150%

By the end of 2020, the number of SaaS unicorns in the world exploded to 156, and the combined valuations were increased by 94 percent compared to the previous year, which can be attributed to investment trends that evaluate valuations per ARR more aggressively than in the past.

We can see that the ARR multiple for cloud startups’ valuations compared to the same ARR reaches about x23—a 150% increase in just five years, compared to 2016.

The significant growth in the valuations over ARR for cloud and SaaS companies can be attributed to a rapid rebound in business expectations in the shadow of COVID-19, and a significant improvement in the unit economics due to the retention of existing customers and increased net dollar retentions. I’ll soon explain this in more detail.

Was COVID-19 a tailwind or a headwind?

Several industry reports analyze cloud-based SaaS or B2B businesses and show that business performance has recovered rapidly in the fall of 2020, compared to the spring of 2020, when COVID-19 had frozen startup investment sentiments.

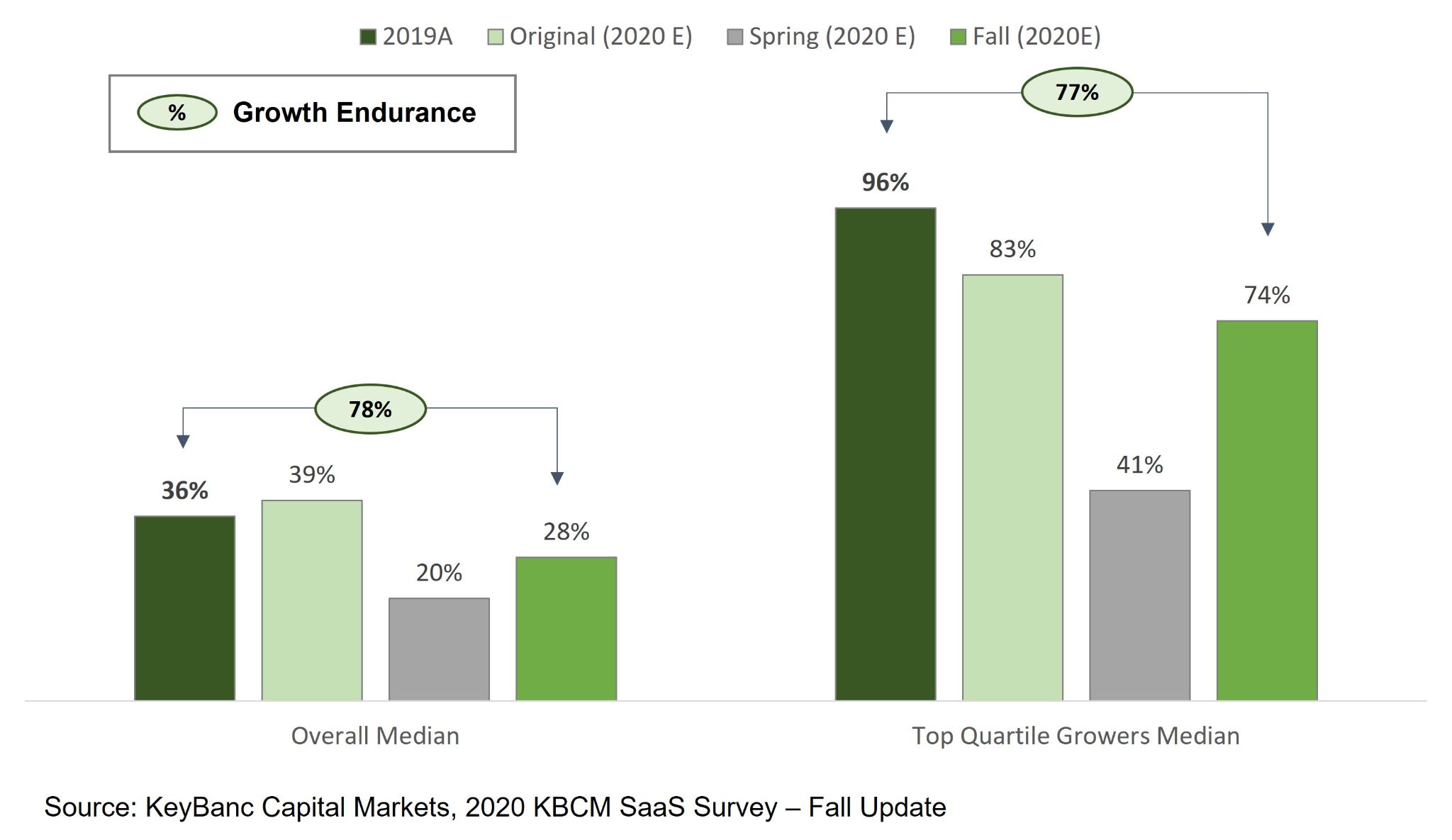

Growth Endurance

It is worth paying attention to the indicator called ‘Growth Endurance’ in the chart above. It is an indicator of dividing the annual (YoY) ARR growth rate of this year by the annual (YoY) ARR growth rate of the previous year. It was introduced as a new paradigm in ‘The State of Cloud,’ published by Bessemer Venture Partners in March 2021.

It’s a new indicator of how steadily the company has grown, and it demonstrates that the market has become more obsessed with startup growth through the COVID crisis. According to the report, public cloud startups recorded growth endurance of about 80% on average, and private companies showed 70–75%. In other words, it appears that growth has been recovered to pre-COVID-19 levels.

Improved quality of growth due to the higher logo and net dollar retention

Between January and June 2020, many companies shifted their sales and marketing strategies from “acquiring new customers” to “retaining existing customers.” This reduced sales and marketing costs in operating expenses for SaaS companies (from 40% in 2018 to 30% in 2020, Openview Partners).

Their efforts to maintain and further upsell existing customers have paid off, and Net Dollar Retention has been restored, enabling companies to improve their business economics, such as increasing loyalty to existing customers and developing product roadmaps based on actual customer requests. In addition, since the demand for cloud-based SaaS has rapidly recovered from the second half of 2020, many SaaS companies were able to kill two birds with one stone: improving the unit economics and generating gross new bookings.

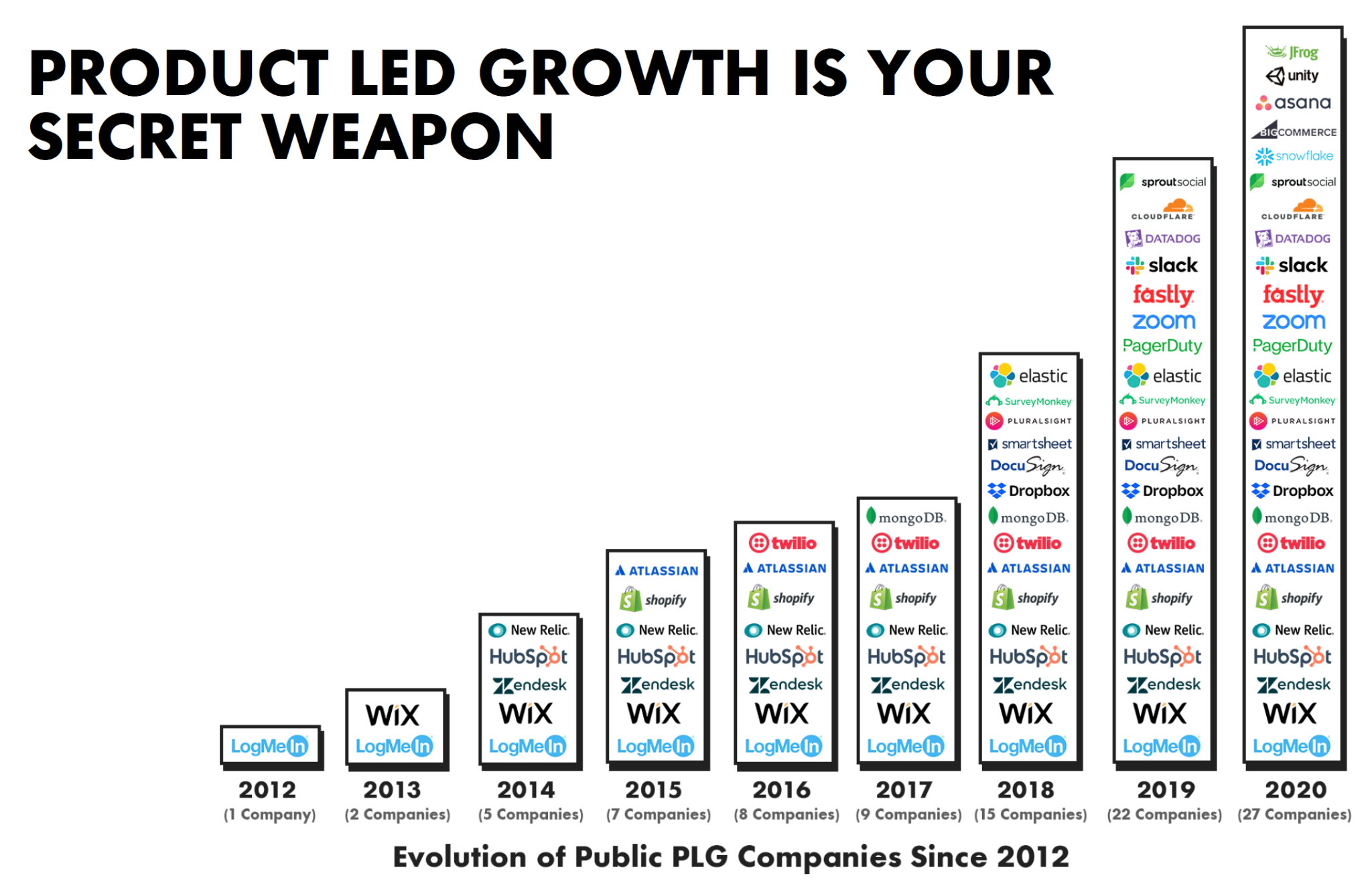

Extending the adoption of ‘Product-led Growth’

Product-led growth is an SaaS growth strategy centered on the product that enables more organic account customer acquisition, paid conversion, and expansion. Investors, including Openview Partners and Bessemer Venture Partners, have supported this strategy for the past few years, and they state that product-led growth gets widely adopted because it lowers the entry barriers for pricing and avoids budget cuts, especially in the COVID-19 era.

Examples of product-led growth include ‘free-trial pricing,’ ‘in-product onboarding processes,’ ‘decision making through product analytics,’ ‘introduction of self-service product buying experience,’ ‘bottom-up sales,’ and ‘adoption of product qualified leads into the sales funnel.’

Breakthrough customer acquisition and net dollar retention using ‘usage-based pricing’

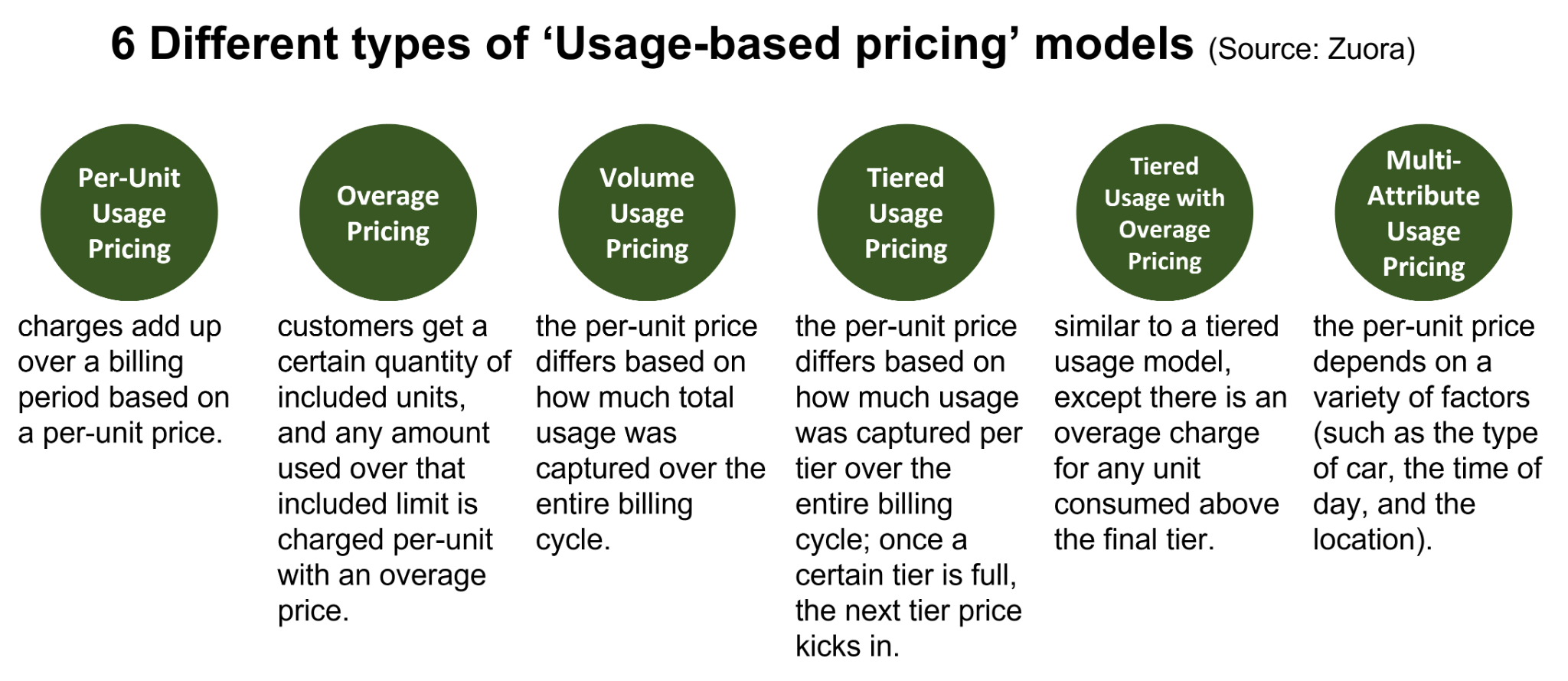

Subscription-based pricing, which provides the different pricing tiers by the segmented product usage level or by the different feature offerings, has been a key strategy for SaaS pricing. However, as the most successful cloud-based B2B and SaaS companies such as Agora, Snowflake, and Datadog have been experiencing remarkable success through ‘usage-based pricing’ for a few years, many SaaS startups are paying attention to this new pricing approach.

As illustrated in the image above, there are about six different types of ‘usage-based pricing,’ but the concept can be simplified into one statement: Contract a certain amount in advance and pay as much as you use. If you run out of balance afterward, you can contract a new one.

Because ‘Usage-based pricing’ lowers the ‘initial barrier to entry’ and can reasonably defend against customer churn, it is rapidly being introduced not only to SMB SaaS but also to the software companies with enterprise-sales motion. There is one caveat, however: because there is no solution that perfectly automates the billing processes to accurately measure product usage and calculate the correct amount for billing without mistakes, companies using legacy systems are forced to deal with a significant amount of manual work.

Recently, startups such as ‘Metronome (https://getmetronome.com/)’ are emerging to solve this problem. We’ll continue to look beyond 2021 to see if this can lead to other market opportunities.

Different SaaS categories, different growth levers

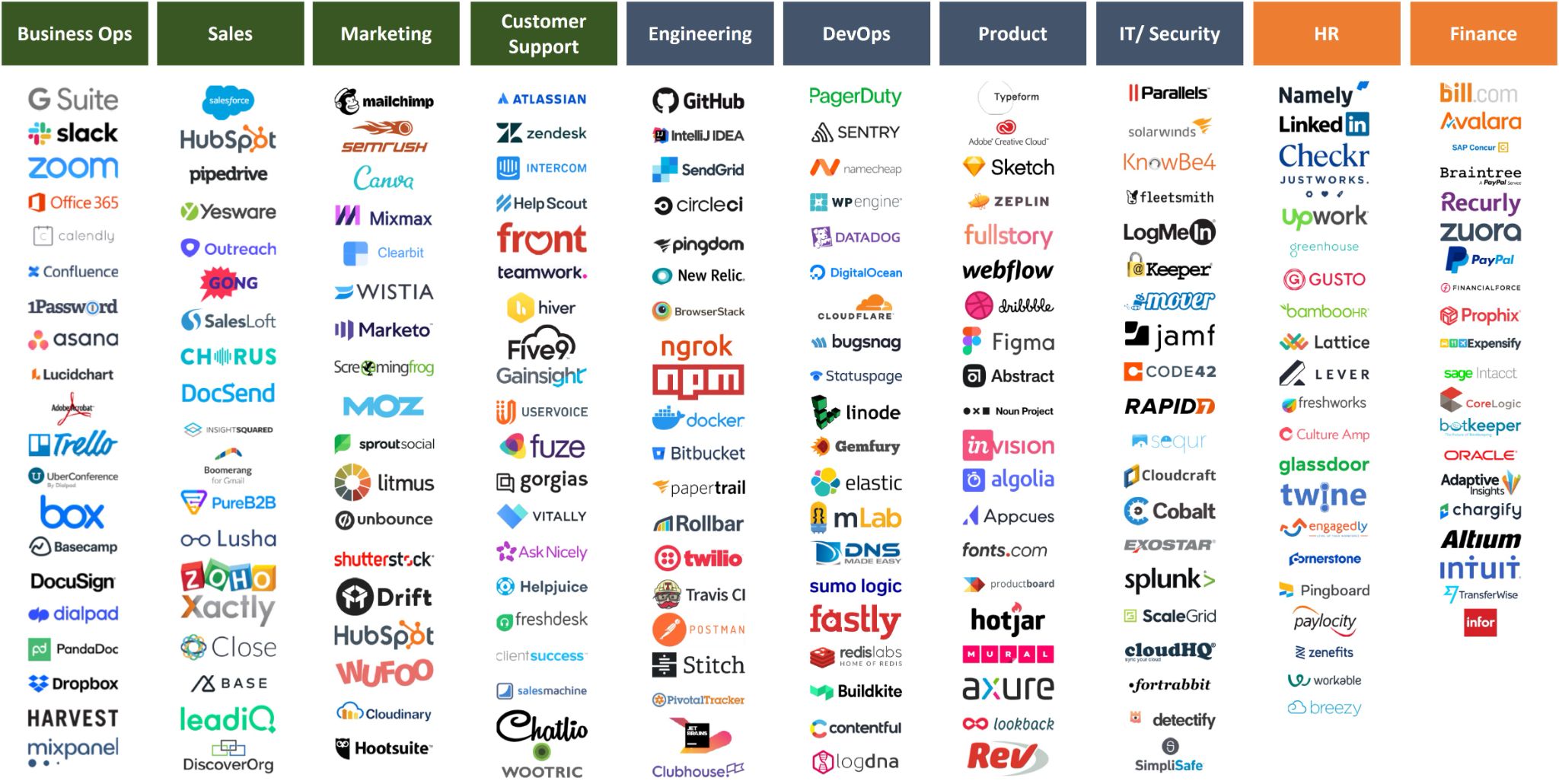

Being explained earlier, many cloud-based B2B, SaaS companies had their sales rebounded rapidly, which is attributable to high demand from the market. There are many categories of cloud-based SaaS businesses: sales and marketing, product/engineering and DevOps, business operations, HR, and finance.

Let’s examine at six trends that survived the COVID-19 crisis in early 2020 and successfully rebounded, enabling explosive sales growth and increased startup valuations.

I. Continuing SaaS Decentralization: the driver to grow the entire SaaS market

IT department is responsible for purchasing software in many companies in the past and still today. However, in the last 5 years, the trend of purchasing the software directly from each working department has been increasing, hence the size of the entire SaaS market is growing rapidly, as companies and departments that have not previously purchased SaaS are starting to purchase.

IT & Security: As many companies are rushing to purchase cloud-based SaaS, which has resulted in the increasing demand for SaaS that helps IT and security departments. Due to the trend of employees working from home or remotely, the number of software systems people use and purchase has become more diverse., As a result, passwords and security management (e.g., SSO) have become important, and the demand for software to comply with recently increased security and privacy compliances (e.g., GDPR, CCPA, etc) is increasing.

Customer Support: Efforts to digitize call center-based customer support services have existed in the past, but the actual investment has been slow because it is difficult for each company to change the existing system and customer support operation procedure. COVID-19 has accelerated the active transformations into digital customer support, so the digital customer support-related software market has grown significantly.

Product and Engineering: Companies that cut their initial hiring plan due to COVID-19 are belatedly starting the hiring again, and the battle for talent is becoming a global phenomenon. As a result, many companies gravitate towards reducing their dependence on manpower by introducing API and DevOps tools as much as possible. In addition, many companies are building offshore engineering teams in a wide range of regions around the world to ensure effective staffing, which also leads to the rapid growth of product and development-related collaboration tools.

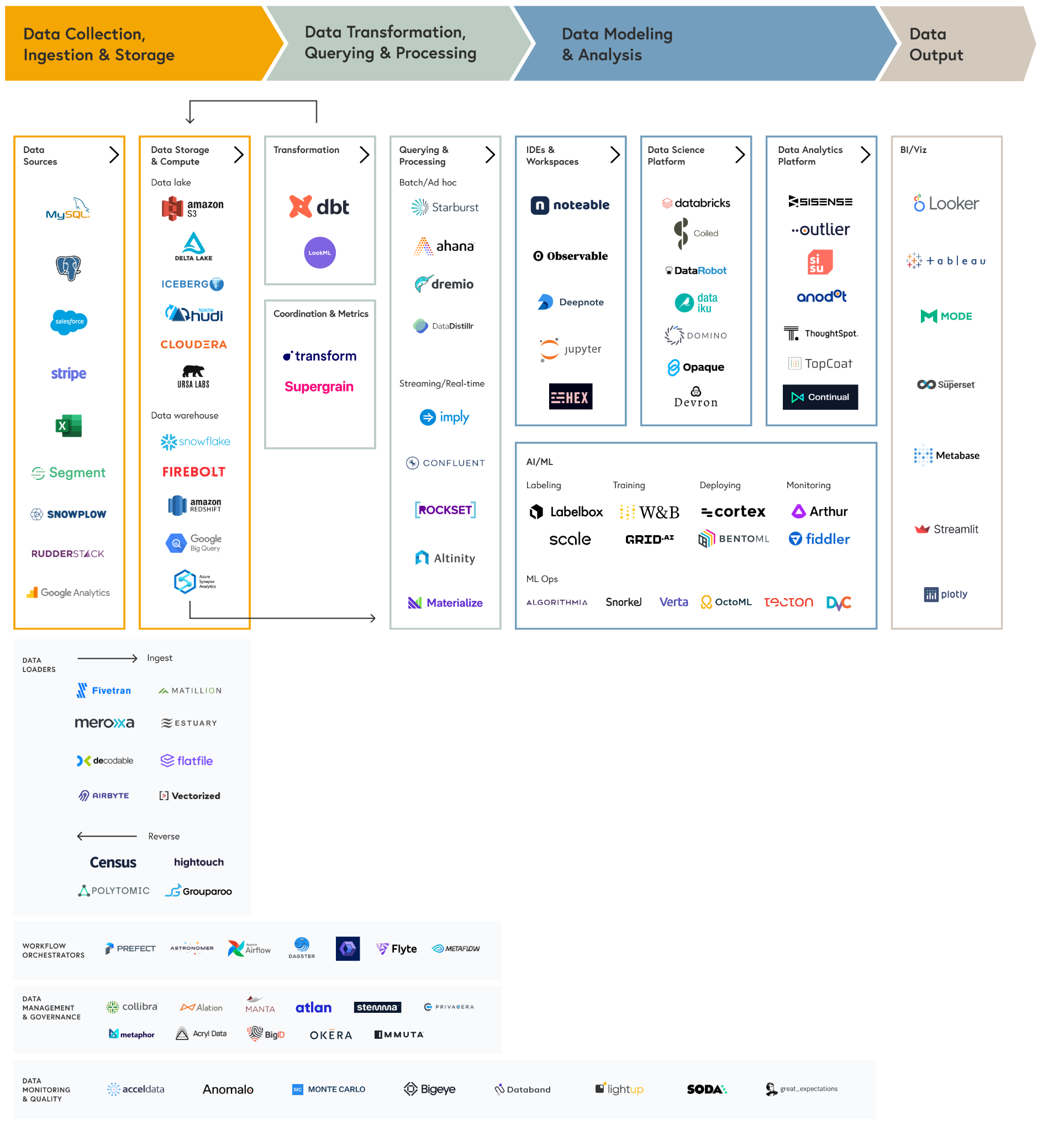

II. The change in cloud-based data tech stacks to handle the explosive increase of data volume

Among all SaaS or cloud-based tools, the market for data infrastructure-related software is exploding. As many companies change their digital infrastructure to cloud-based, fundamental data tech stack changes are required to more efficiently handle the vast amount of data. In addition to the engineering staff handling complex data, the demand for people handling the daily data needs is also growing competitively; accordingly, the trend to build fully software-driven, SaaS-based data systems is expected to continue.

III. The rapid rise of DEI tools in the human resources area

There is a growing demand for a variety of tools to pursue diversity in the human resources field and to strengthen cultural homogeneity and cohesion in remote working situations. This is called ‘Diversity, Equity, and Inclusion (DEI),’ and it shows that a new paradigm is becoming a mainstream trend beyond the traditional HR practices of recruitment, training, compensation, and evaluation.

IV. The movement of O2O (Offline-to-Online) industries from platform-centric to SaaS-centric

The self-employed were known as the last demand group for digital transformation because most of their transactions take place offline, and it was not easy for them to preemptively invest in digital transformation. Recently, as the group is moving online to survive COVID-19, various software areas are growing rapidly to help them switch and operate their businesses online.

In addition, in the past, such digital transformation had been dependent on major platform providers (e.g., Facebook, Kakao, Line), whereas Direct-to-Consumers (D2C) is an emerging trend that enables a direct connection to consumers by allowing them to build their own websites or applications. D2C allows self-employed people to deviate from the platform, and the decentralization of digital platforms is clearly observed.

V. Vertical SaaS becomes a more solid trend

Cloud-based digital transformation trends are rapidly evolving, providing specialized offerings for each industry. Vertical SaaS software powering detailed industry categories is emerging. About 31 Vertical SaaS startups have already been listed publicly, and their value is about $653 Bn as of 2020—up 820% from a decade ago. These include Procore in construction, ServiceTitan in maintenance and repair, Shopmonkey in auto repair, Squire in Barbershop Point of Sale and Management System, and GlossGenius in salon & spa.

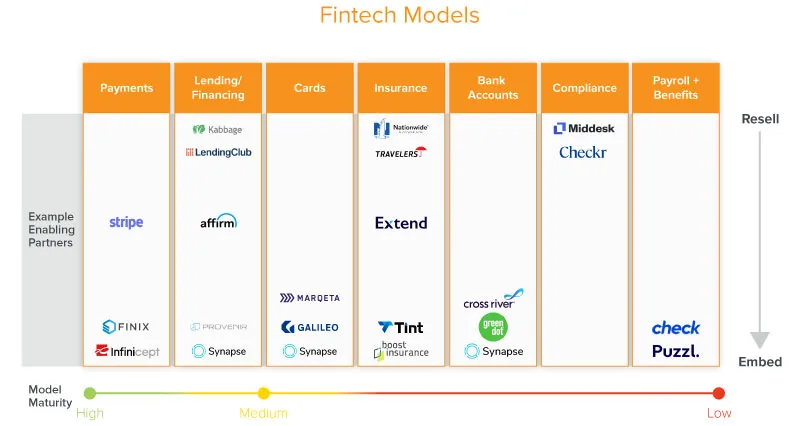

VI. The new paradigm of Fintech, providing infrastructure for integrated services

Driven by the growth of vertical SaaS and the trend of decentralization that allows businesses to serve consumers on their own instead of relying on giant platforms, the trend of providing fintech services such as bank accounts, loans, payments, payrolls, taxes, and settlement has given rise to new opportunities.

Banking as-a-service: Banking as-a-service allows businesses to issue and manage bank accounts through a business operator (e.g., Shopify) without having to use a bank. Some partners (e.g., Synapse, GreenDot) can help to activate bank accounts.

B2C payments: This is by far the most common and widely adopted service category. Here, many software companies—including Shopify, Mindbody, Tast, ServiceTitan, Clio, and Brightwheel—have achieved vertical integration of consumer-to-consumer payment processing.

B2B payments: Despite the slow adoption specific to the B2B sector, new payment-related APIs have been introduced to accelerate the digitization of B2B payments (e.g., restaurants 365, GHX, Textura).

Payrolls: The Payrolls sector is still dominated by major existing players such as ADP. As ServiceTitan provides new solutions in the field of home repair and maintenance, more vertical SaaS innovations are expected in the future.

Credit card issuance: Software such as Stripe, Privacy, Marqueta, and Galileo act as card issuance platforms, helping software companies to issue debit cards more easily.

Loan: It seems a natural strategy for SaaS companies that have data on cash flow and solvency of their client companies to extend their business models to loans.

Concluding ‘Discover Cloud 2021’

The growth of cloud-based B2B and SaaS startups is a global trend. However, in contrast to the ‘decentralization’ mentioned several times in this report, the thought leadership on the cloud is led by the limited numbers of Silicon Valley VCs, so I wanted to give an outside-in perspective to the cloud and SaaS industry.

Since this is the first edition of the annually planned report of ‘Discover Cloud,’ it has many limitations, as it mainly cites external analysis rather than direct analysis. I hope to include more independent analysis and insight in the future.

2 thoughts on “Discover Cloud 2021: Read global cloud trends 2021”